16

2025

-

05

Economic Operation Analysis of the Sewing Machinery Industry in Q1 2025

In the first quarter of 2025, the global economy exhibited a complex and volatile landscape amidst multiple risks and uncertainties. Factors such as rising trade protectionism, ongoing geopolitical conflicts, and differentiated inflationary pressures intertwined, accelerating the restructuring of global supply chains. Driven by US tariff policies and their anticipated impact, US consumption and import replenishment needs were brought forward, and the phenomenon of various countries rushing to export textiles and garments effectively boosted China's sewing machinery exports. Industry enterprises seized opportunities and challenges, accelerating market structural adjustments. Supported by strong external demand, the industry's operation continued the steady progress of the previous year, achieving a stable start to the economy.

1. Overall stable industry operation, gradual improvement in corporate profits

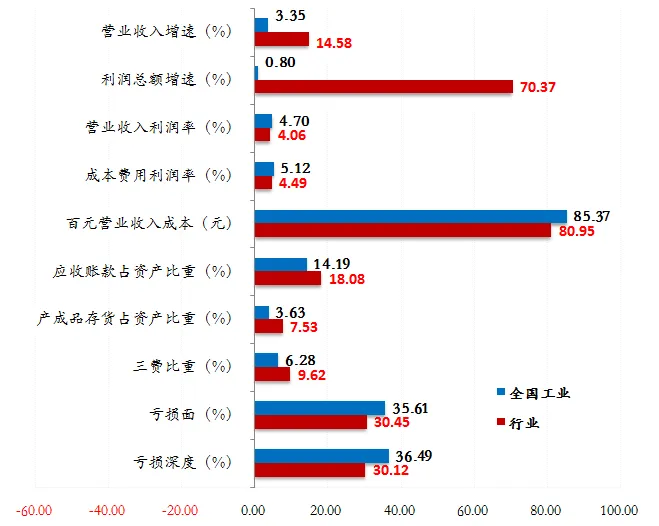

In the first quarter of 2025, the industry's production and sales scale grew steadily, and the level of corporate profits gradually improved. Data from the National Bureau of Statistics shows that in the first quarter of 2025, 289 large-scale enterprises in the industry achieved an operating income of 8.3 billion yuan, a year-on-year increase of 14.58%, with a total profit of 340 million yuan, a year-on-year increase of 70.37%; the operating income profit margin was 4.06%, an increase of 1.33 percentage points compared to the same period last year; the cost per 100 yuan of operating income was 80.95 yuan, a decrease of 1.81 yuan compared to the same period last year; and the three-expense ratio was 9.62%, a decrease of 0.81 percentage points compared to the same period last year. According to the association's statistics of 100 major complete machine enterprises, the cumulative operating income of 100 complete machine production enterprises in the industry in the first quarter reached 6.315 billion yuan, a year-on-year increase of 9.08%; and the total profit reached 490 million yuan, a year-on-year increase of 28.77%.

In the first quarter, the industry's loss ratio narrowed, and operating efficiency showed steady improvement, but problems such as increased losses and high accounts receivable continued to emerge. Data from the National Bureau of Statistics shows that in the first quarter, the loss ratio of large-scale enterprises in the industry was 30.12%, a decrease of 10 percentage points compared to the same period last year; the loss amount was 102 million yuan, a year-on-year increase of 9.17%, an increase of 85 million yuan compared to the same period last year; and the industry's loss depth was 30.12%, a decrease of nearly 17 percentage points compared to the same period last year. The finished product turnover rate of large-scale enterprises increased by 8.43% year-on-year, the total asset turnover rate increased by 9.75% year-on-year, and the accounts receivable turnover rate increased by 9.48% year-on-year. Accounts receivable of large-scale enterprises reached 7.1 billion yuan, a year-on-year increase of 4.65%, and the ratio of accounts receivable to assets reached 18.08%, an increase of 0.04 percentage points compared to the same period last year, higher than the national average of 14.19 for large-scale industrial enterprises.

Figure 1 Operating conditions of large-scale enterprises in the industry in the first quarter of 2025

(Data source: National Bureau of Statistics)

2. Slight increase in production, slight increase in industrial machine inventory

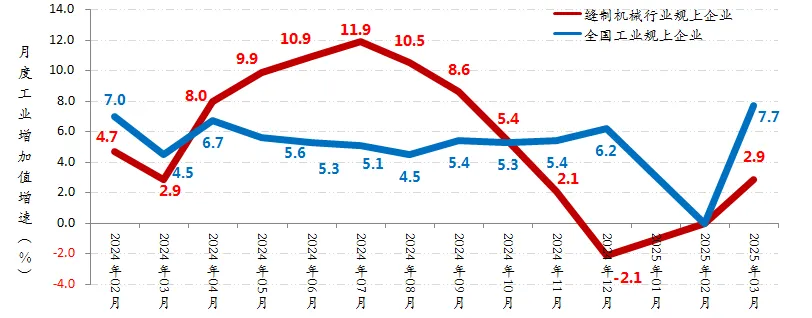

In the first quarter of 2025, the industry's overall production continued its positive growth trend, but the growth rate slowed significantly compared to the end of last year. Data from the National Bureau of Statistics shows that the monthly industrial added value growth rate of large-scale enterprises in the industry in the first quarter was positive, with the monthly industrial added value growth rate in March reaching 2.9%, and the cumulative industrial added value growth rate reaching 8.2%, higher than the national average of 6.5% for large-scale industrial enterprises in the same period.

Figure 2 Changes in the monthly industrial added value of large-scale enterprises in the industry

(Data source: National Bureau of Statistics)

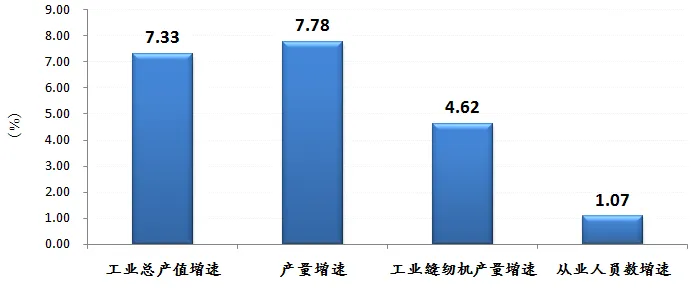

According to the association's statistics of 100 major complete machine production enterprises, the total industrial output value of 100 enterprises in the industry in the first quarter reached 5.4 billion yuan, a year-on-year increase of 7.33%; the total output of sewing equipment reached 1.68 million units, a year-on-year increase of 7.78%. Among them, the output of industrial sewing machines reached 1.15 million units, a year-on-year increase of 4.62%. Except for overlock machines, the quarterly output of major product categories showed varying degrees of year-on-year growth. At the end of March, the number of employees in 100 enterprises increased by 1.07% year-on-year.

Figure 3 Growth rate of major production indicators of 100 major complete machine production enterprises in the industry from January to March 2025

(Data source: China Sewing Machinery Association)

From the perspective of monthly industry and industrial sewing machine production, in January, driven by external demand, the output of industrial sewing machines by 100 major complete machine production enterprises in the industry reached 385,000 units, a year-on-year increase of 3.51% and a month-on-month decrease of 18.31%. In February, affected by the Spring Festival holiday, the output of industrial sewing machines by 100 enterprises in the industry dropped to 331,000 units, a year-on-year increase of 19.19%. In March, with the full resumption of work and production by enterprises, the release of accumulated order demand, and the impact of increased shipments in the foreign trade market, the industry's output increased rapidly, with the output of industrial sewing machines by 100 enterprises reaching 439,000 units, a year-on-year decrease of 6.21% and a month-on-month increase of 32.38%.

Figure 4 Monthly output of industrial sewing machines by 100 major complete machine production enterprises in the industry in the past three years

(Data source: China Sewing Machinery Association)

From the perspective of industry inventory, at the end of March, the finished goods inventory of 289 large-scale enterprises in the industry increased by 3.36% year-on-year, and the total inventory of 100 major complete machine production enterprises in the industry was approximately 660,000 units, a year-on-year decrease of 1.19%. Among them, the inventory of industrial sewing machines was 510,000 units, a year-on-year increase of 5.42%, and the inventory of industrial sewing machine products in the industry showed a slight increase compared to the same period last year.

3. Slowdown in downstream production and demand, significant decline in domestic sales of sewing equipment

In the first quarter of 2025, China's series of policies to stabilize growth continued to exert their effects, and the steady economic development trend continued to be consolidated. However, under the influence of weak consumption and US tariff policies, the order volume of upstream industries such as spinning and dyeing decreased, and the shoe and clothing processing and consumer markets became sluggish. Affected by the reduction and relocation of foreign trade orders, the closure of small and medium-sized garment processing factories increased, a large number of second-hand sewing equipment flowed out, further impacting the market, and the wait-and-see attitude of downstream shoe and clothing enterprises intensified. According to statistics from the National Bureau of Statistics, the output of large-scale garment enterprises in China in the first quarter increased by only 1.8% year-on-year, a decrease of 2.42 percentage points compared to 2024; garment exports amounted to US$33.01 billion, a year-on-year decrease of 1.9%; and the retail sales of clothing, shoes, hats, needles, and textiles in above-scale units increased by 3.4% year-on-year, with the growth rate continuing to narrow. At the same time, although the production, sales, and exports of related downstream industries such as shoes and hats, home textiles, bags, and home furnishings maintained single-digit or slight growth, they all faced challenges such as a continuous slowdown in growth rate and shrinking investment.

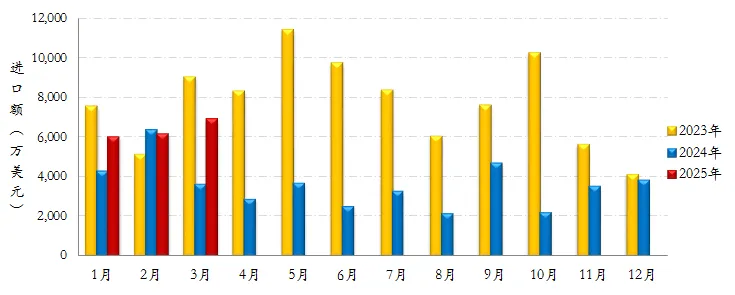

Under the unfavorable situation of a general slowdown in production, sales, and exports in major downstream industries, domestic sales of sewing equipment in China showed a significant decline. According to preliminary estimates, domestic sales of sewing equipment in China in the first quarter decreased by about 25% year-on-year. According to the latest data from the customs, in the first quarter, China imported 6,934 industrial sewing machines, with an import value of US$16.25 million, a year-on-year decrease of 35.80% and 43.82% respectively, which further indirectly confirms the unfavorable situation of sluggish domestic demand.

Figure 5 Amount of imported sewing machinery products in the industry in the past three years

(Data source: General Administration of Customs)

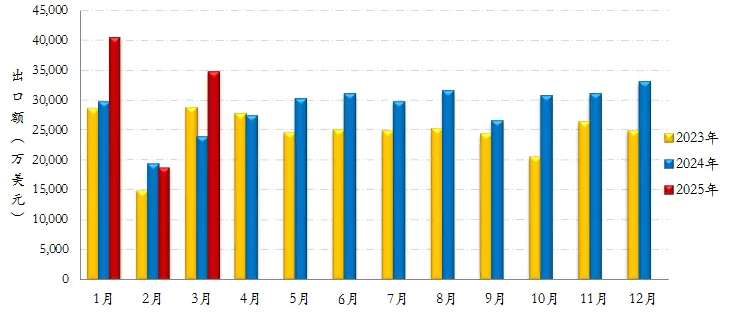

4. Significant increase in exports, reaching a new historical high for the same period

In the first quarter of 2025, affected by the combined factors of inventory replenishment demand and the rush to export, the demand in overseas markets such as South Asia, ASEAN, Africa, and Latin America continued to be released, driving a significant increase in China's sewing machinery exports. By the end of March, China's cumulative export value of sewing machinery products reached US$935 million, a year-on-year increase of 28.87%, reaching a new historical high for the same period, and the industry's foreign trade started off well.

From the monthly export data, the industry continued its growth momentum from last year in January, with exports reaching US\$403 million, a year-on-year increase of 36.14% and a month-on-month increase of 22.18%, setting a new record high for monthly export value. Subsequently, in February, affected by factors such as the Spring Festival holiday, the industry's export value dropped to US\$186 million, a year-on-year decrease of 3.43% and a month-on-month decrease of 53.88%. In March, China's sewing machinery exports reached US\$346 million, a year-on-year increase of 46.05% and a month-on-month increase of 86.35%. The low base effect coupled with the rush to export were the main factors driving the increase in export growth this month.

Figure 6: Export Value of Sewing Machinery Products in the Industry Over the Past Three Years

(Data source: General Administration of Customs)

In terms of export products, in the first quarter, except for household sewing machines, the export value of various industrial sewing machines and their components showed growth to varying degrees. Among them, the export volume of industrial sewing machines was 1.24 million units, with an export value of US\$426 million, a year-on-year increase of 22.86% and 29.89% respectively; the export volume of embroidery machines was 25,500 units, with an export value of US\$201 million, a year-on-year increase of 19.79% and 57.42% respectively (among them, the export volume of embroidery machines with an average price of over US\$2,000 was 15,600 units, with an export value of US\$193 million, a year-on-year increase of 25.07% and 53.88% respectively); the export volume of pre- and post-sewing equipment was 460,000 units, with an export value of US\$139 million, a year-on-year increase of 29.33% and 24.66% respectively; the export value of components was US\$113 million, a year-on-year increase of 14.61%; the export volume of household sewing machines was 2.06 million units, a year-on-year increase of 1.60%, with an export value of US\$55.6 million, a year-on-year decrease of 6.66% (among them, the export volume of household sewing machines with an average price of over US\$22 was 980,000 units, a year-on-year increase of 1.79%, with an export value of US\$45.64 million, a year-on-year decrease of 4.87%).

Figure 7: Classification of China's Sewing Machinery Product Exports in the First Quarter of 2025

(Data source: General Administration of Customs)

In terms of export prices, in the first quarter of 2025, the export prices of industrial sewing machines and embroidery machines in China showed a year-on-year increase. Among them, the average export price of industrial sewing machines was US\$343.9 per unit, a year-on-year increase of 5.72%; the average export price of embroidery machines was US\$7,906.7 per unit, a year-on-year increase of 31.41%.

Table 1: Average Export Prices of Major Sewing Machinery Products in China in the First Quarter of 2025

(Unit: USD/unit, %)

(Data source: General Administration of Customs)

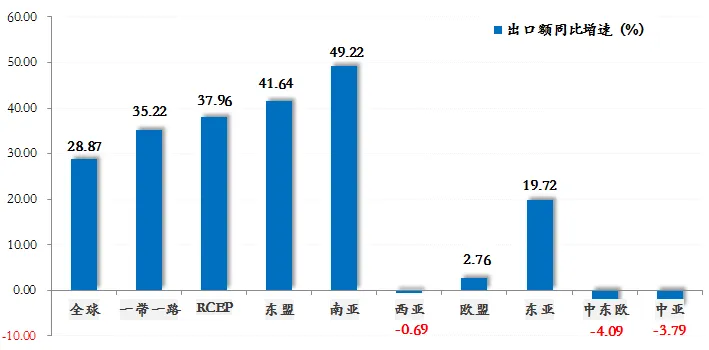

From the perspective of key export markets, in the first quarter, China's exports of sewing machinery products to the four major key markets of Asia, Africa, Latin America, and North America all showed significant growth, while exports to Europe and Oceania continued to decline year-on-year. Among the various regional markets, China's exports to the "Belt and Road" market reached US\$683 million, a year-on-year increase of 35.22%, accounting for 73.06% of the industry's export value, an increase of 3.43 percentage points compared to the same period last year; exports to the RCEP market reached US\$295 million, a year-on-year increase of 37.96%, accounting for 31.52% of the industry's export value, an increase of 2.08 percentage points compared to the same period last year; exports to the South Asian market reached US\$280 million, a year-on-year increase of 49.22%, accounting for 30.00% of the industry's export value, an increase of 4.09 percentage points compared to the same period last year; exports to the ASEAN market reached US\$263 million, a year-on-year increase of 41.64%; exports to the West Asian market reached US\$62.95 million, a year-on-year decrease of 0.69%; exports to the North African market reached US\$49.31 million, a year-on-year increase of 65.68%; exports to the EU market reached US\$32.74 million, a year-on-year increase of 2.76%; exports to the East Asian market reached US\$29.57 million, a year-on-year increase of 19.72%; exports to the Central Asian market reached US\$17.83 million, a year-on-year decrease of 3.79%.

Figure 8: Major Export Regions of China's Sewing Machinery Products in the First Quarter of 2025

(Data source: General Administration of Customs)

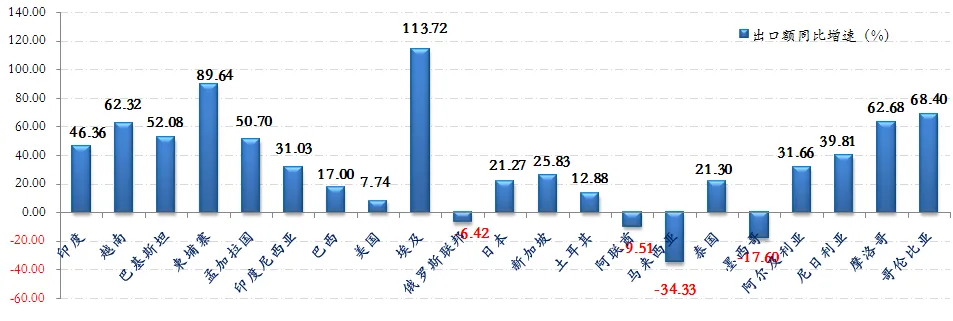

Specifically, in terms of countries, in the first quarter, among the 192 countries and regions to which China exported sewing machinery products, nearly 60% of the markets showed positive year-on-year growth in export value. The top six export markets (India, Vietnam, Pakistan, Cambodia, Bangladesh, and Indonesia) all showed significant year-on-year growth in export value. Among the top 20 export markets, only 4 markets showed negative year-on-year growth in export value. Among them, 10 markets showed a year-on-year growth rate of over 30%, and 6 markets showed a year-on-year growth rate of over 50%. Exports to Egypt showed a doubling of growth. Among the top 20 export markets, four are in Africa: Egypt, Algeria, Nigeria, and Morocco.

India remains China's largest export market for sewing equipment. From January to March, China's cumulative exports of sewing machinery products to India reached US\$171 million, a year-on-year increase of 46.36%, accounting for 18.28% of China's industry export value; exports to Vietnam reached US\$121 million, a year-on-year increase of 62.32%, accounting for 12.93% of China's industry export value; exports to Pakistan reached US\$52.88 million, a year-on-year increase of 52.08%, accounting for 5.66% of China's industry export value. In addition, China's exports of sewing machinery products to ASEAN markets such as Cambodia, Indonesia, Thailand, and Myanmar; African markets such as Egypt, Algeria, Nigeria, Morocco, Kenya, and Ghana; Latin American markets such as Brazil, Colombia, Peru, and Argentina; and regional markets such as the United States, Japan, and Singapore all showed year-on-year growth. Among them, exports to Egypt, Argentina, Portugal, New Zealand, and Honduras all showed a doubling of year-on-year growth. However, exports of sewing machinery products to regional markets such as Russia, the UAE, Malaysia, Mexico, and the Philippines, as well as to the Middle Eastern markets of Iran and Iraq, and the Central Asian regional markets of Kyrgyzstan and Kazakhstan, showed a year-on-year decline.

Table 2: Export of Sewing Machinery Products by Country and Region in the First Quarter of 2025

(Unit: USD, %)

(Data source: General Administration of Customs)

Figure 9: Growth of Major Export Markets for China's Sewing Machinery Products in the First Quarter of 2025

(Data source: General Administration of Customs)

Overall, in the first quarter, domestic demand for China's sewing machinery industry was sluggish, while external demand continued to grow. Sewing machinery companies seized the opportunity to accelerate their overseas expansion, taking measures such as participating in overseas international sewing equipment exhibitions and increasing investment in marketing and service resources to further accelerate the optimization of domestic and foreign market layouts. Supported by strong external demand, the industry achieved a stable start overall.

Looking ahead to the second quarter, the international economic and trade environment is experiencing the most complex situation and the most profound changes since China's accession to the WTO. Under the impact of the US's imposition of reciprocal tariff policies on multiple countries around the world and related expectations, global economic growth and industrial chains and supply chains are facing enormous challenges. Although tariff games and great power games have currently experienced dramatic and phased easing and adjustments, the uncertainty of US government policies and the subsequent development of tariff policies will still profoundly affect global economic and development expectations. The trend of restructuring the global supply chains of downstream industries such as textiles and apparel is irreversible, and will also have a profound impact on the future economic development and market layout of China's sewing machinery industry. It is expected that during the favorable window period of the temporary suspension of reciprocal tariffs by the US and the simultaneous reduction of US-China tariffs, downstream industries such as textiles, apparel, shoes, hats, and bags in various countries, including China and Southeast Asia, will accelerate capacity expansion and rush to export, and the demand for sewing equipment will generally remain stable. Under the unfavorable situation of increasing wait-and-see attitudes in both domestic and foreign markets, China's sewing machinery industry's production and exports are expected to continue the development trend of the first quarter, with domestic demand continuing to decline and external demand slowing down. The industry's economy is expected to remain basically flat compared to last year.

Recommendation

Add: F/101, Building 1, Zone 3, Yongyuan Small and Micro Enterprise Park, No.555 Yongyuan Road, Lunan Street, Luqiao District, Taizhou City

E-mail:chenhonglie2015@sina.com

E-mail:515189516@qq.com

Scan to enter the phone terminal

© Taizhou HORLEY Sewing Machine Co., Ltd. SEO Business license