21

2025

-

05

Analysis of the current situation of China's industrial sewing machine industry, and a positive outlook for the development of the sewing machinery industry

PART ONE

Overview of the Industrial Sewing Machine Industry

I. Overview of the Industrial Sewing Machine Industry An industrial sewing machine is a sewing machine suitable for mass production of sewn workpieces in sewing factories or other industrial sectors. Factories that require sewing machines, such as clothing and hat factories, all use industrial sewing machines.

1. Classification

In actual work, the names of industrial sewing machines are mostly named based on the number of needles and threads, stitch type, and degree of automation. Examples include single-needle chain stitch machines, five-thread overlock machines, and three-needle five-thread coverstitch machines. According to the degree of usage, they are divided into three major categories: general-purpose sewing machinery, special-purpose sewing machinery, and special sewing machinery.

2. Development History

In China, sewing machines were initially called “iron cars”, “foreign machines”, “needle cars”, etc. The last emperor, Puyi, once gave Empress Wanrong a Singer sewing machine, which was a rare item in China at the time. After the founding of the People's Republic of China in 1949, the sewing machinery industry developed significantly. The industry underwent restructuring and transformation phases, including public-private partnerships and mergers, resulting in reasonable division of labor and the formation of a number of backbone enterprises: such as Shanghai's Qie, Chang, Huigong, Feiren, Hudie, and Tianjin Sewing Machine Factory, as well as Guangzhou's South China Sewing Machine Factory, etc. These sewing machine manufacturers mainly produced ordinary household sewing machines and low-end industrial sewing machines. By 2004, there were more than 600 sewing machine manufacturers and more than 1,000 parts manufacturers in China, with an annual output of 14.008 million units, a total output value of approximately 28 billion yuan, and nearly 1,000 varieties. China has become one of the world's major sewing machinery producing countries.

PART TWO

Industrial Sewing Machine Industry Development Environment

1. Relevant Policies

The State Council and relevant departments continue to issue relevant industrial policies to encourage and guide the development of the sewing machinery industry, driving the transformation and upgrading of China's traditional manufacturing industry and promoting China's entry into the ranks of a “manufacturing powerhouse”.

2. Business Climate

In 2022, the development of China's sewing machinery industry faced significant challenges, with the overall economy slowing down and declining quarter by quarter. From the end of 2021 to 2022, the industry's business climate index fell from the overheating range, hovering in the stable and gradually cooling ranges, and finally fell to the overcooling range in December. In December, the comprehensive business climate index was 77.62, the lowest point in nearly two years. Among them, the main business income business climate index was 83.53, the export business climate index was 71.22, the asset business climate index was 96.99, and the profit business climate index was 58.26. Among the four indexes, only the asset business climate index was in the stable range, the main business income business climate index was in the gradually cooling range, and the export and profit indexes were both in the overcooling range, putting increasing pressure on the industry's development.

Relevant Report: Published by Huajing Industry Research Institute “2024-2030 China Industrial Sewing Machine Industry Development Operation Status and Investment Strategy Planning Report”

PART THREE

Industrial Sewing Machine Industry Chain

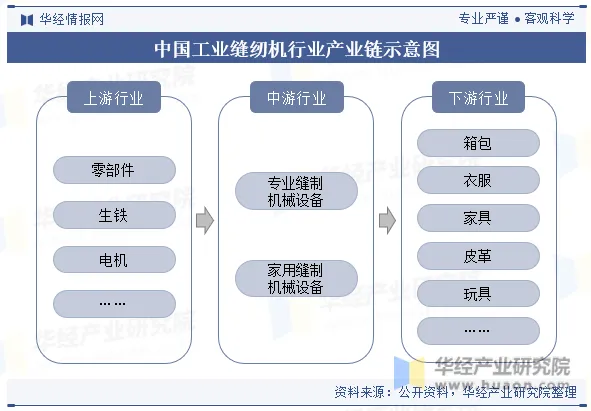

1. Industrial Chain

The upstream of the industrial sewing machine industry is the raw material and component industry, mainly including pig iron, servo motors, and other components; the midstream is industrial sewing machinery equipment manufacturers; and the downstream is the application areas of industrial sewing machines, including luggage, clothing, furniture, leather, toys, and other fields.

2. Upstream Industry Market Size

The upstream of the sewing machine industry's industrial chain mainly consists of pig iron and motor industries. A servo motor is an engine that controls the operation of mechanical components in a servo system, acting as an auxiliary motor for indirect speed change. Servo motors can control speed, with very accurate positional accuracy, converting voltage signals into torque and speed to drive the controlled object. In recent years, the market size of China's servo motor industry has continued to expand, reaching 18.1 billion yuan in 2022, a year-on-year increase of 7.1%.

PART FOUR

Current Status of the Industrial Sewing Machine Industry

1. Market Size

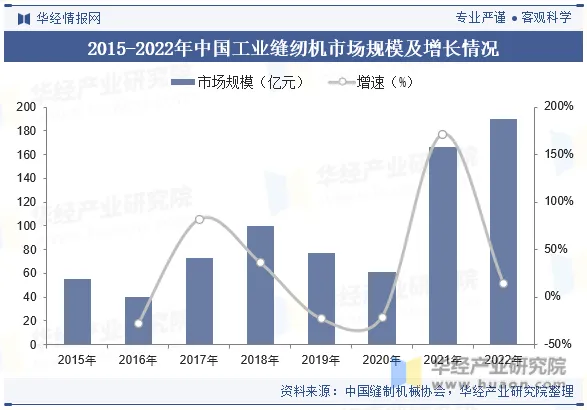

The textile industry is an important part of China's national economy. In recent years, China's textile industry has developed well, driving the healthy development of China's sewing machine industry. In 2021, the Chinese sewing machine market size experienced explosive growth, reaching 16.619 billion yuan, a year-on-year increase of 171.42%; in 2022, the market size reached 19 billion yuan, a year-on-year increase of 14.33%.

2. Output

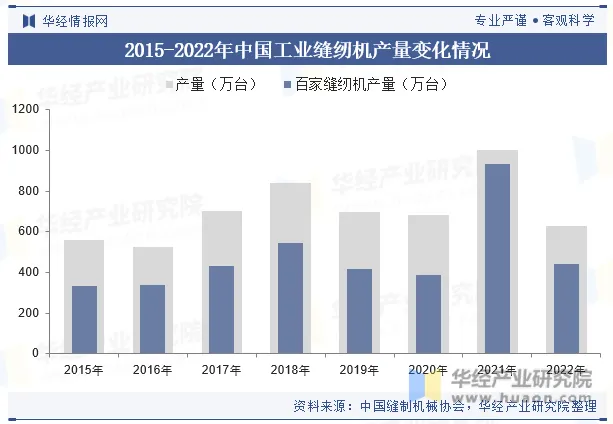

From the perspective of China's industrial sewing machine output, from 2017 to 2022, driven by product upgrades and improvements in the downstream industry's business climate, China's sewing machine output showed significant volatility. In 2021, the output reached 10 million units, with 9.33 million units produced by 100 sewing machine manufacturers, both the highest values in recent years. In 2022, the total output of industrial sewing machines across the industry was approximately 6.3 million units, returning to the level of 2020. In 2022, more than 100 key whole-machine manufacturers under the association's statistics produced a total of 4.41 million industrial sewing machines. China's industry still has approximately 800,000-900,000 industrial sewing machines in inventory, a significant reduction in inventory pressure compared to the end of the previous year. However, under the current slowdown in domestic and foreign demand and the downturn in the economy, some inventory products are unsold, and the pressure to reduce inventory remains substantial.

3. Domestic Sales

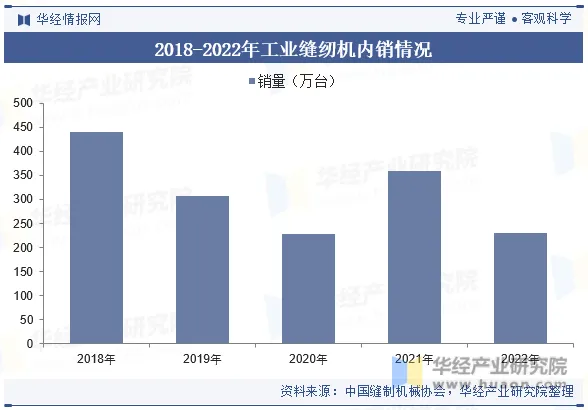

In 2022, the domestic sales environment for sewing equipment in China was severe, remaining weak since the beginning of the year, with demand showing a cliff-like decline in the second and third quarters. In 2022, the total domestic sales of industrial sewing equipment in the industry were approximately 2.3 million units, a year-on-year decrease of 36.1%. The market returned to the relatively low level of 2020.

4. Export Volume

The export volume of China's industrial sewing machines has maintained an upward trend since 2012, showing a fluctuating upward trend due to the cyclical nature of the industry. From January to September 2023, China's industrial sewing machine exports totaled 777,200 units.

Note: The compiled data is for non-household automatic flat sewing machines (84522110)

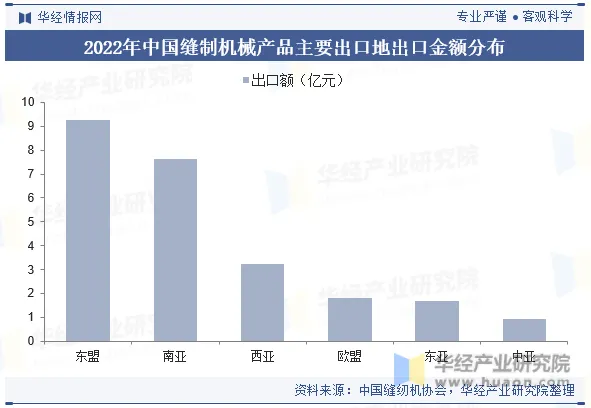

5. Export Destinations

In various regional markets in 2022, China's exports to ASEAN totaled US\$925 million; to South Asia, US\$764 million; to West Asia, US\$3.25 million; to the EU, US\$1.82 million; to East Asia, US\$168 million; and to Central Asia, US\$95 million.

6. Market Segmentation

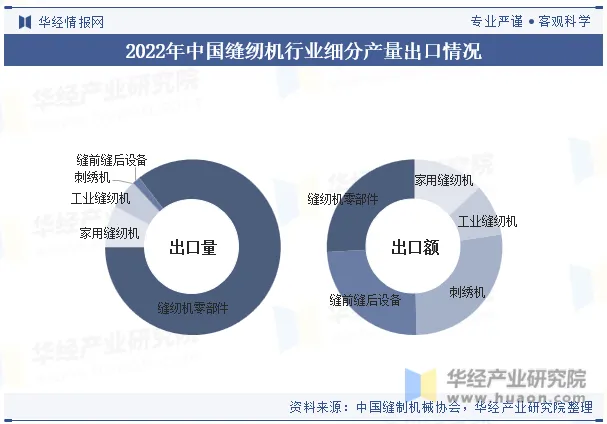

In the Chinese sewing machinery market, industrial sewing machines dominate, accounting for 60.52% of total output in 2022. Multi-functional household sewing machines and ordinary household sewing machines follow, with shares of 17.29% and 15.37%, respectively. In 2022, the total output of industrial sewing machines across China was approximately 6.3 million units, a year-on-year decrease of 37%; household sewing machine output was approximately 3.4 million units, down 32% year-on-year, with ordinary household machines at approximately 1.6 million units (down 33.33%) and multi-functional household machines at approximately 1.8 million units (down 30.77%). Output of pre- and post-sewing equipment (including cutting, cloth pulling, ironing, etc.) reached 710,000 units, a year-on-year increase of 35.98%.

PART 5

Competitive Landscape of the Industrial Sewing Machine Industry

1. Competitive Landscape

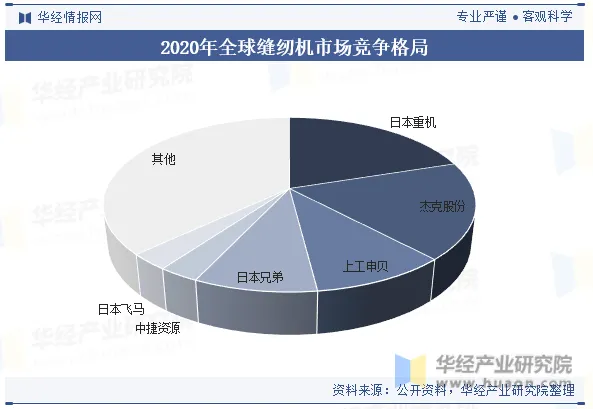

Major overseas companies include Japan Juki, Brother Industries (Japan), and PFAFF (Japan). Major domestic companies include Jack Sewing Machine, Shanggong Shenbei, Standard Sewing Machine, and Zhongjie Resources. Based on over 80 years of refined operation and technological accumulation, Japan Juki holds a leading position in sewing machinery equipment. The company is a first-tier manufacturer in Japan, ranking second globally in market share in 2020 (18%).

2. Key Enterprises

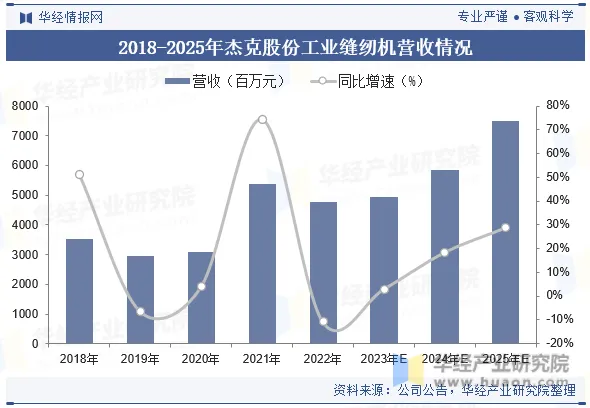

In 2022, the revenue from industrial sewing machine products of Jack Sewing Machine, Shanggong Shenbei, Standard Sewing Machine, and Zhongjie Resources was as follows: Jack Sewing Machine's revenue reached 4.78 billion yuan, far exceeding the second-place Zhongjie Resources' 867 million yuan, approximately 5.5 times higher.

Jack Sewing Machine held an 18% market share in 2020, ranking second globally, only behind Japan Juki's 20% share. Jack Sewing Machine's domestic market share is also continuously increasing. In 2022, its industrial sewing machine product revenue reached 4.78 billion yuan, several times higher than that of other domestic competitors in the same business. From 2018 to 2022, the company's revenue and net profit attributable to the parent company showed compound annual growth rates of 7.29% and 2.13%, respectively, indicating relatively stable operations. Affected by cyclical adjustments in the industry, the first quarter of 2023 saw year-on-year decreases of -6.7% and -2.71%, respectively, but the decline has narrowed further, and full-year performance is expected to turn positive.

PART 6

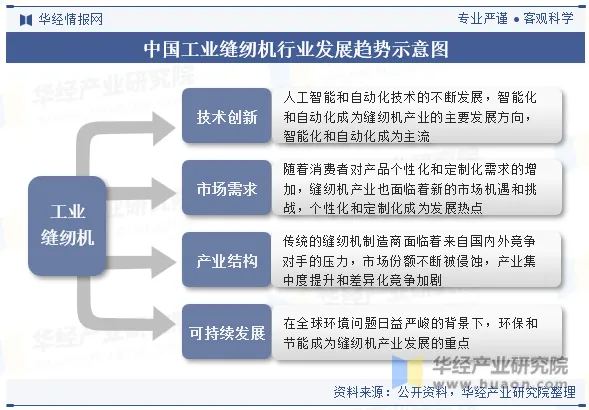

Future Development Trends of the Industrial Sewing Machine Industry

Sewing machines, as traditional textile equipment, have played a vital role in the textile industry since their inception. With continuous technological advancements, the sewing machine industry is constantly evolving, with new technologies and designs driving innovation and development. Intelligence and automation, personalization and customization, increased industry concentration, and environmental protection and energy saving will be future development trends in the sewing machine industry. Sewing machine manufacturers need to increase R\&D investment, improve product technology content and competitiveness, and meet the opportunities and challenges of industry development.

Recommendation

Add: F/101, Building 1, Zone 3, Yongyuan Small and Micro Enterprise Park, No.555 Yongyuan Road, Lunan Street, Luqiao District, Taizhou City

E-mail:chenhonglie2015@sina.com

E-mail:515189516@qq.com

Scan to enter the phone terminal

© Taizhou HORLEY Sewing Machine Co., Ltd. SEO Business license