22

2024

-

11

Analysis of the Sewing Machinery Industry's Economic Operation in the First Three Quarters of 2024

In the first three quarters of 2024, the global economy maintained a slow recovery, inflation pressure eased significantly, developed economies such as the US and Europe successively launched interest rate cut cycles, consumer power and inventory replenishment demand gradually released, and the business climate of manufacturing industries in regions such as South Asia, ASEAN, and Africa continued to improve. China successively introduced a package of policy incentives to stabilize the economy and expand domestic demand, and the development expectations of consumption, investment, and production gradually improved, creating favorable internal and external conditions for the stable development and transformation and upgrading of the sewing machinery industry.

After two consecutive years of decline in the industry economy, 2024 ushered in a cyclical growth momentum of bottoming out and rebounding. In the first three quarters, China's sewing machinery industry seized the opportunity of rising downstream demand and cyclical development, actively implemented the "three products" strategy, actively explored domestic and foreign markets, accelerated digital transformation, and on the basis of a low base in the previous year, the main indicators of the industry's production, sales, exports, and benefits all turned from negative to positive year-on-year, market vitality and business confidence actively recovered, achieving a good start for restorative growth and high-quality development.

I. The operation of the industry economy in the first three quarters of 2024

1. Significant improvement in benefits, stable recovery of quality and efficiency

In the first three quarters of 2024, the industry's production and sales scale rebounded rapidly, leading to a significant improvement in enterprise quality and efficiency. According to data from the National Bureau of Statistics, in the first three quarters, 275 large-scale production enterprises in the industry achieved operating income of 23.8 billion yuan, a year-on-year increase of 18.64%, an increase of 0.63 percentage points compared with the first half of the year; the total profit reached 1.132 billion yuan, a year-on-year increase of 61.05%, an increase of 3.72 percentage points compared with the first half of the year; the operating profit margin was 4.76%, a year-on-year increase of 35.75%, down 0.27 percentage points compared with the first half of the year. The cost per 100 yuan of operating income for large-scale enterprises was 81.76 yuan, down 1.07% year-on-year; the three-expense ratio for large-scale enterprises was 9.85%, down 5.01% year-on-year.

In the first three quarters, the loss rate of the industry further narrowed, and the operating efficiency of enterprises steadily recovered. By the end of September, the loss rate of large-scale enterprises in the industry was 24%, a narrowing of 3.57 percentage points compared with the first half of the year; the loss amount increased by 11.57% year-on-year, and the loss depth was 18.48%, an expansion of 1.27 percentage points compared with the first half of the year. The finished product turnover rate and total asset turnover rate of large-scale enterprises in the industry increased by 26.75% and 17.18% year-on-year respectively; the amount of accounts receivable was 7.3 billion yuan, down 4.10% year-on-year, accounting for 30.75% of current operating income, a narrowing of 16.75 percentage points compared with the first half of the year, higher than the average of 25.93% for large-scale industrial enterprises nationwide in the same period.

Figure 1 Operating conditions of large-scale enterprises in the industry in the first three quarters of 2024

(Data source: National Bureau of Statistics)

2. Moderate growth in production, continuous optimization of inventory

Driven by the recovery of demand and inventory replenishment, the overall production of the industry showed a restorative growth trend in the first three quarters. According to data from the National Bureau of Statistics, from January to September, the cumulative growth rate of industrial added value of large-scale production enterprises in China's sewing machinery industry reached 8.2%, an increase of 1.2 percentage points compared with the growth rate in the first half of the year, higher than the cumulative growth rate of 5.2% for large-scale enterprises in the manufacturing of light industrial production special equipment in the same period, and also higher than the average cumulative added value of 5.8% for large-scale industrial enterprises nationwide in the same period.

Figure 2 Changes in the cumulative added value growth rate of large-scale enterprises in the industry from September 2023 to September 2024

(Data source: National Bureau of Statistics)

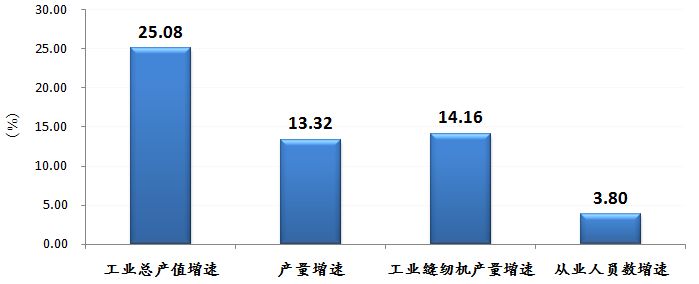

According to the data of 100 complete machine enterprises compiled by the association, in the first nine months, the total industrial output value of 100 enterprises in the industry was 14 billion yuan, a year-on-year increase of 25.08%; the output of sewing equipment was 4.53 million units, a year-on-year increase of 13.32%; and the output of industrial sewing machines was 3.16 million units, a year-on-year increase of 14.16%. Among them, conventional machine types such as computer flat bed sewing machines, overlock machines, sergers, heavy-duty machines, and embroidery machines all showed double-digit moderate growth, while template machines and automatic machines showed medium-high speed growth. The number of employees in 100 enterprises at the end of September increased by 3.80% year-on-year.

Figure 3 Growth rate of major production indicators of 100 complete machine production enterprises in the industry from January to September 2024

(Data source: China Sewing Machinery Association)

From the monthly production of industrial sewing machines by 100 complete machine enterprises in the industry, the industry's production in the first three quarters of 2024 increased significantly compared with the previous year. In January, enterprises actively replenished inventories and increased exports, and the output of industrial sewing machines by 100 enterprises in the industry remained at 403,000 units. In February, affected by the Spring Festival holiday, the output of industrial sewing machines by 100 enterprises fell to 269,000 units. In March, with the full resumption of work and production by enterprises, the release of accumulated order demand, and the faster recovery of domestic and foreign trade markets in some regions, the output of industrial sewing machines by 100 enterprises increased significantly to 482,000 units. In the second and third quarters, affected by the moderate decline in market demand, the output of industrial sewing machines by 100 enterprises in the industry slightly decreased in April and then rebounded moderately again, with production stabilizing at around 400,000 units. In September, the output of industrial sewing machines by 100 enterprises in the industry was 439,000 units, a year-on-year increase of 11.15%.

Figure 4 Monthly output of industrial sewing machines by 100 enterprises in the industry in recent three years

(Data source: China Sewing Machinery Association)

In the first three quarters of 2024, the inventory of sewing equipment in the industry showed an overall downward trend. The inventory of sewing equipment of 100 complete machine enterprises in the industry decreased from nearly one million units at the end of last year to 740,000 units at the end of June, and then to 660,000 units at the end of September (including 470,000 units of industrial sewing machines), a year-on-year decrease of 17.45%, and the industry's effect of clearing inventory and reducing inventory was significant, and the inventory structure continued to be optimized.

3. Domestic demand clearly warmed up, sales were high in the beginning and low at the end

In the first three quarters, the national series of steady growth policies gradually exerted their efforts, and the development expectations of downstream industries such as clothing improved positively, and investment demand and per capita clothing consumption expenditure increased. The demand in traditional markets such as the United States and the European Union remained resilient, which provided positive support for the stable development of production and export in downstream industries such as domestic clothing, home textiles, footwear, and luggage. The domestic phased equipment procurement demand was quickly released in the first half of the year. Regions such as Dehong, Baoshan, and Honghe in Yunnan actively undertook the transfer of textile and garment industries from inland areas, and equipment procurement demand surged. At the same time, backbone complete machine enterprises in the sewing machinery industry increased research and development and promotion of efficient and intelligent equipment, participated in professional exhibitions, held new product launches, strengthened technical services, focused on the publicity and preferential sales of small and fast, large-scale products, and carried out activities such as trade-ins, in order to further increase brand marketing at the terminal and strive to leverage the existing market.

According to incomplete surveys and statistical calculations, on the basis of a relatively low base in the previous year, the domestic sales of industrial sewing equipment by backbone complete machine enterprises in China all achieved double-digit moderate growth in the first three quarters. From a quarterly perspective, the growth of domestic sales in the industry was significant in the first quarter. In the second and third quarters, affected by factors such as consumption, orders, inventory, and labor costs, users began to adopt a cautious wait-and-see attitude towards the market, and the demand for traditional sewing equipment by clothing factories decreased significantly, while the procurement demand for template machines and automatic machines remained strong, and the growth rate of domestic sales in the industry slowed down.

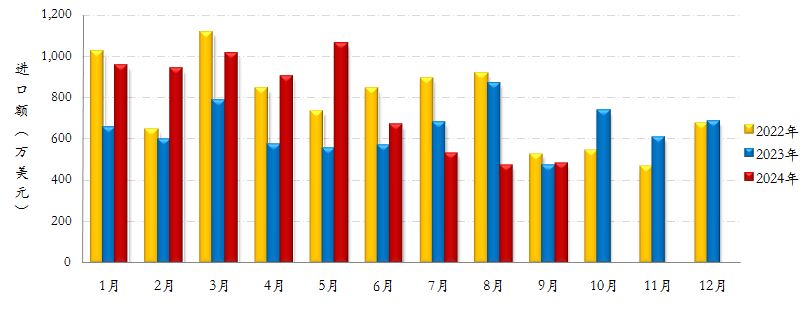

According to the latest data from customs, in the first three quarters, China's import volume of industrial sewing machines was 41,000 units, and the import value was US$69.76 million, a year-on-year increase of 41.36% and 22.32% respectively; the import value of sewing machine parts was US$62.48 million, a year-on-year increase of 43.99%, showing that the recovery of downstream industries in China has released a large market demand for high-end special sewing equipment and automated equipment.

Figure 5 Recent three-year monthly import amount of industrial sewing machine products

(Data Source: General Administration of Customs)

4. Exports are steadily recovering, and major markets are showing strong growth

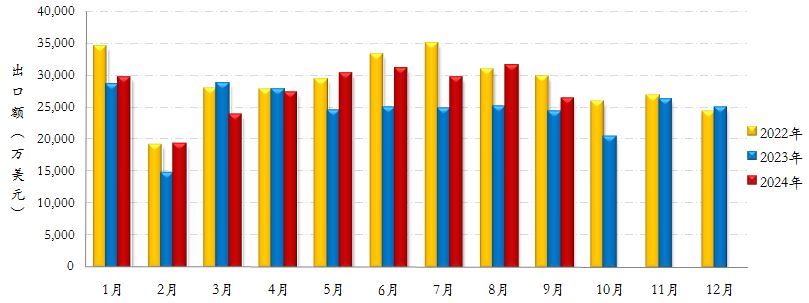

In the first three quarters, with the steady recovery of the global economy and the release of replenishment demand for shoes and clothing in developed economies, market demand in some regions such as South Asia, ASEAN, Africa, and Latin America has warmed up. Vietnam, India, Cambodia, Pakistan, Egypt, Brazil and other key overseas markets for shoe and clothing production and exports have generally achieved recovery growth, effectively driving a steady recovery in the export of Chinese sewing machinery products. According to data from the General Administration of Customs: In the first three quarters, China's cumulative exports of sewing machinery products amounted to US\$2.479 billion, an increase of 13.25% year-on-year.

From the monthly export trend, since December 2023, the monthly export growth rate of China's sewing machinery industry has turned positive. In January, the industry's export value was US\$296 million, a year-on-year increase of 3.86%; in February, affected by factors such as the Spring Festival holiday, the industry's export value dropped to US\$192 million, but still increased by 30.77% year-on-year; in March, under the general environment of repeated global inflation and tight credit, the industry's export value was US\$237 million, a year-on-year decrease of 17.24%, showing a trend of contraction at the end of the quarter; in the second and third quarters, the prosperity of the global manufacturing industry and international trade continued to improve, and overseas market demand for sewing machinery products gradually recovered. From May to August, the average monthly export value of the industry remained above US\$300 million, achieving a steady recovery. At the end of the third quarter, the global economy continued to recover, but the growth momentum weakened. Affected by factors such as increasing uncertainty in international trade, escalating geopolitical conflicts, the US election, and the gradual weakening of the labor market in major economies such as Europe and the United States, the subsequent momentum of global consumption was slightly insufficient, and downstream users gradually fell into a wait-and-see situation. The industry's monthly export value fell to US\$260 million, a year-on-year increase of 8.70%, and a month-on-month decrease of 16.28%.

Figure 6 Monthly Export Value of Sewing Machinery Products in the Industry in Recent Three Years

(Data Source: General Administration of Customs)

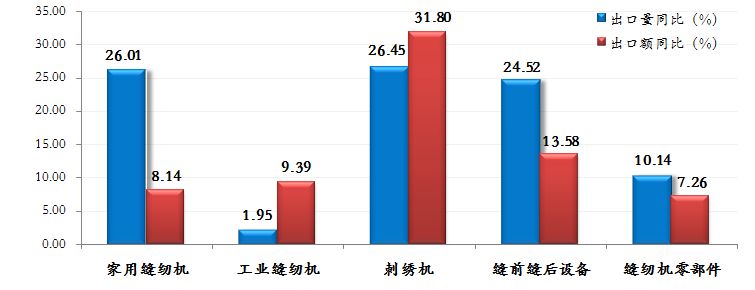

From the perspective of export products, in the first three quarters, China's exports of industrial sewing machines amounted to 3.46 million units, with an export value of US\$1.114 billion, an increase of 1.95% and 9.39% respectively year-on-year. Among them, the export volume of automatic sewing machines was 2.31 million units, with an export value of US\$814 million, an increase of 4.38% and 13.47% respectively year-on-year. The proportion of automatic products in industrial sewing machines was 66.86% and 73.11% respectively in terms of quantity and value, which increased by 1.55 and 2.63 percentage points respectively compared with the same period last year; the export volume of embroidery machines was 71,000 units (including products below US\$2,000), with an export value of US\$472 million, an increase of 26.45% and 31.80% respectively year-on-year; the export volume of pre- and post-sewing equipment was 1.49 million units, with an export value of US\$356 million, an increase of 24.52% and 13.58% respectively year-on-year; the export value of sewing machine parts was US\$325 million, an increase of 7.26% year-on-year; the export volume of household sewing machines was 7.94 million units (including manual sewing machines), with an export value of US\$212 million, an increase of 26.01% and 8.14% respectively year-on-year. Exports of all major product categories in the industry showed growth.

Figure 7 Year-on-Year Change in Export Indicators of China's Classified Sewing Machinery Products in the First Three Quarters of 2024

(Data Source: General Administration of Customs)

From the perspective of export prices, in the first three quarters, the export average prices of industrial sewing machines and embroidery machines in China showed a year-on-year growth trend. Among them, the average export price of industrial sewing machines was US\$322.3/unit, a year-on-year increase of 7.29%; the average export price of embroidery machines was US\$6,649.2/unit, a year-on-year increase of 4.24%. However, the average export prices of household sewing machines and pre- and post-sewing equipment showed a downward trend year-on-year.

Table 1 Export Average Prices of Major Categories of Sewing Machinery Products in China in the First Three Quarters of 2024

(Unit: USD/unit, %)

(Data Source: General Administration of Customs)

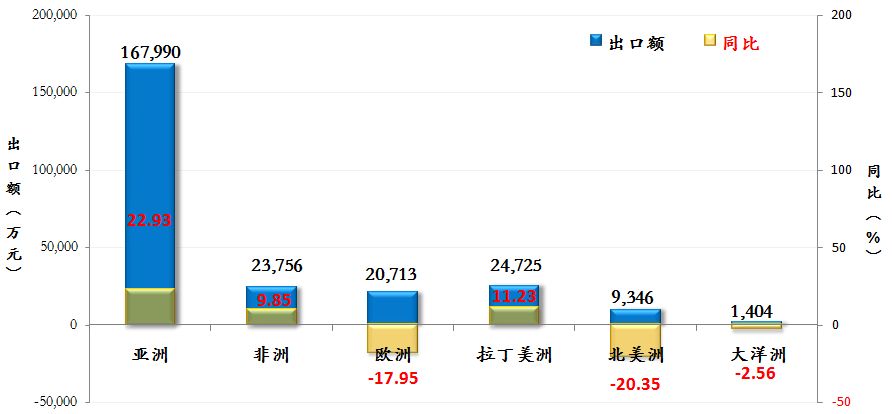

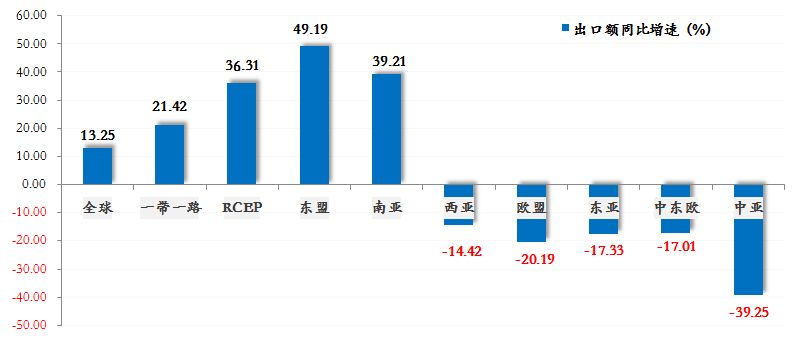

From the perspective of key export regions, in the first three quarters of 2024, China's exports of sewing machinery products to Asia, Latin America, and Africa showed growth, while exports to Europe, North America, and Oceania showed a year-on-year decline. Among the various regional markets, China's exports to the "Belt and Road" market amounted to US\$1.73 billion, a year-on-year increase of 21.42%, accounting for 69.58% of the industry's total exports, an increase of 4.68 percentage points compared with the same period last year; exports to the RCEP market amounted to US\$737 million, a year-on-year increase of 36.31%, accounting for 29.74% of the industry's total exports, an increase of 5.03 percentage points compared with the same period last year; exports to the ASEAN market amounted to US\$647 million, a year-on-year increase of 49.19%, accounting for 26.10% of the industry's total exports, an increase of 6.29 percentage points compared with the same period last year; exports to the South Asian market amounted to US\$645 million, a year-on-year increase of 39.21%, accounting for 26.00% of the industry's total exports, an increase of 4.85 percentage points compared with the same period last year; exports to the West Asian market amounted to US\$194 million, a year-on-year decrease of 14.42%; exports to the EU market amounted to US\$105 million, a year-on-year decrease of 20.19%; exports to the East Asian market amounted to US\$78.81 million, a year-on-year decrease of 17.33%; exports to the Central Asian market amounted to US\$74.65 million, a year-on-year decrease of 39.25%.

Figure 8 China's Exports of Sewing Machinery Products to Major Continents in the First Three Quarters of 2024

(Data Source: General Administration of Customs)

Figure 9 China's Exports of Sewing Machinery Products to Major Markets in the First Three Quarters of 2024

(Data Source: General Administration of Customs)

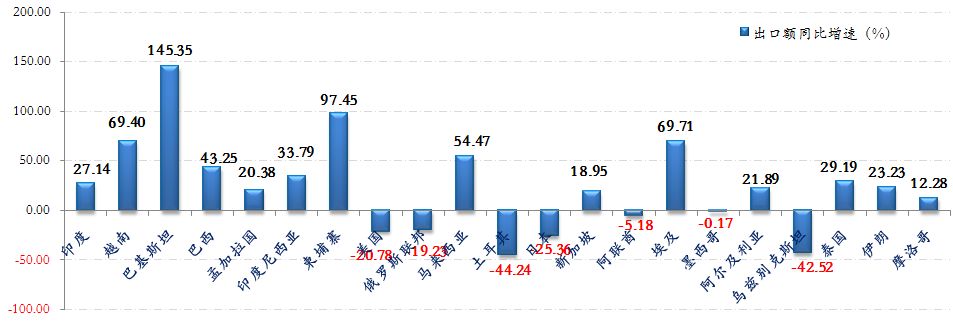

From a country-by-country perspective, in the first three quarters of 2024, among the 203 countries and regions to which China exported sewing machinery products, the export value of more than half of the markets showed positive year-on-year growth. The export value of the top seven export markets in the industry (India, Vietnam, Pakistan, Brazil, Bangladesh, Indonesia, and Cambodia) all showed significant year-on-year growth. Among the top 20 export markets, 13 markets showed positive year-on-year growth in export value. Among them, 7 markets showed a year-on-year growth rate of over 30%, and 1 market showed a year-on-year doubling of export value—Pakistan.

Figure 10 Growth in the Value of China's Exports of Sewing Machinery Products to Major Markets in the First Three Quarters of 2024

(Data Source: General Administration of Customs)

II. Outlook for Industry Economic Operation in the Fourth Quarter of 2024

Overall, in the first three quarters of 2024, driven by the cyclical recovery of domestic and international markets, China's sewing machinery industry has ushered in a positive trend of recovery from its bottom.

In the fourth quarter, according to the latest forecast by the IMF in October 2024, global economic growth is expected to remain stable, and inflation is expected to continue to decline, providing positive conditions for major central banks to ease monetary policy. However, affected by the intensification of major power games, continued geopolitical conflicts, and the slowdown in consumption growth in major economies, the global economic situation remains complex and changeable; under the combined influence of multiple factors, the Chinese economy, relying on the steady release of domestic demand and precise policy adjustment, especially the introduction of a series of incremental policies, will gradually enhance its economic growth momentum, the consumer market will gradually warm up, and the economy is expected to continue to stabilize and recover, laying a solid foundation for achieving the annual GDP growth target of 5%.

From the perspective of the development of downstream industries closely related to sewing equipment, with the weak recovery of the global economy and consumer demand, the apparel, leather, footwear, home textiles, and luggage industries are still in a period of slow recovery, with certain resilience and potential for development. In the fourth quarter, it is expected that the production, sales, revenue, profit, and investment indicators of various downstream industries will continue to maintain a low-speed growth and stable development trend. After the US election, the new government's plan to impose additional tariffs on the global market and China may, in the short term, further stimulate the replenishment demand in Europe and the United States and the short-term benefits of increased production and export grabbing in downstream industries.

In the fourth quarter, China's sewing machinery industry is still expected to maintain relatively stable development. Domestic demand is expected to slow down while export growth will continue, and market growth will further concentrate on various specialized, functional, and automated equipment. Industry enterprises should maintain confidence in development, closely focusing on the strategic requirements of building a modernized industrial system and a new type of productive force, seeking steady progress amid stability, seeking opportunities amid challenges, deeply understanding user pain points, accelerating technological innovation, promoting intelligent transformation, appropriately increasing production to replenish inventory, and focusing on overseas markets. They should continuously strengthen their overall competitiveness and differentiated advantages, promoting high-quality development from the inside out with more proactive strategic measures.

This news is reprinted from: China International Sewing Equipment Exhibition

Recommendation

Add: F/101, Building 1, Zone 3, Yongyuan Small and Micro Enterprise Park, No.555 Yongyuan Road, Lunan Street, Luqiao District, Taizhou City

E-mail:chenhonglie2015@sina.com

E-mail:515189516@qq.com

Scan to enter the phone terminal

© Taizhou HORLEY Sewing Machine Co., Ltd. SEO Business license